Asset Allocation Viewpoints & Positioning Q1 2021

Asset Allocation Viewpoints & Positioning

First Quarter 2021

Actionable investment conclusions from Harbor’s Multi-Asset Solutions Team

Read the updated perspectives here

Macro Landscape

From Recovery To Reflation: Vaccinations, A New Fed Framework, And Fiscal Stimulus Will All Collide In 2021 To Put Upward Pressure On Inflation In the Years to Come

- We’ve revised our U.S. Gross Domestic Product (GDP) growth forecast up from 6.0% to 8.0% in Q4 of 2021 to account for the $1.9T fiscal stimulus measure recently passed.

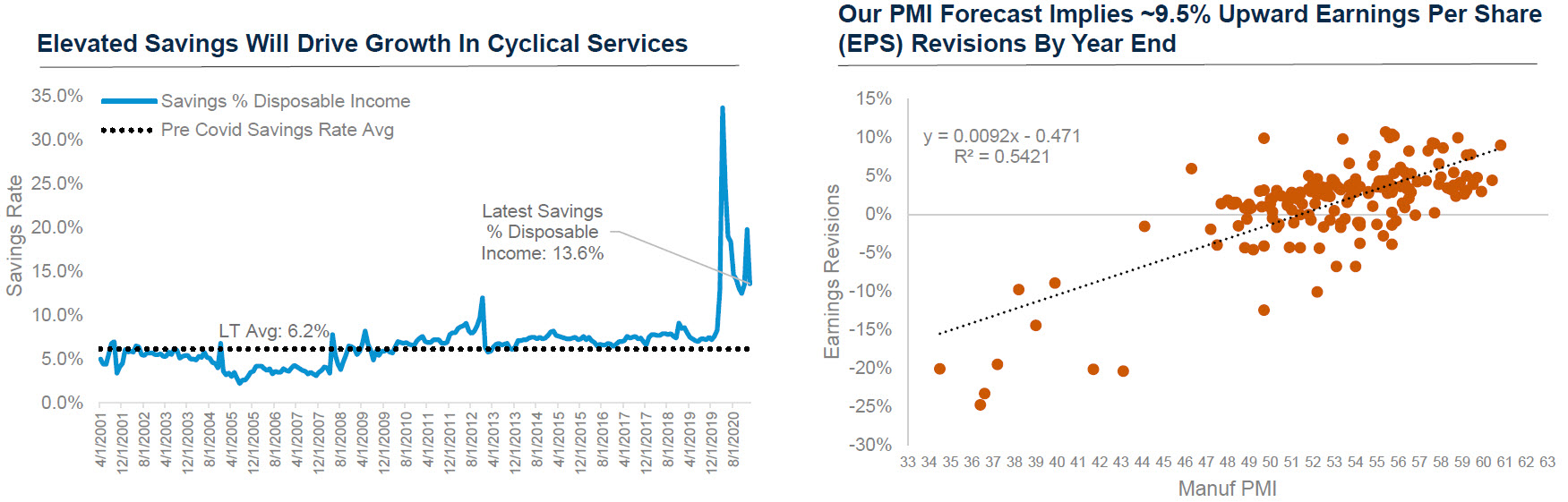

- We believe above trend growth in 2021 will be driven by a re-opening of society beginning in the summer, fiscal stimulus, pent up demand for cyclical services and $1.5T in excess consumer cash balances.

- We are confident that vaccines and natural immunity from prior infection will provide enough protection from severe outcomes as to warrant a re-opening of the U.S. by early summer and Europe by late summer.

- The U.S. has implemented $2.8T of fiscal stimulus in recent months which brings the full tally to $5.3T - and we expect more to come; Democrats have already proposed another $3.0T infrastructure bill for later this year.

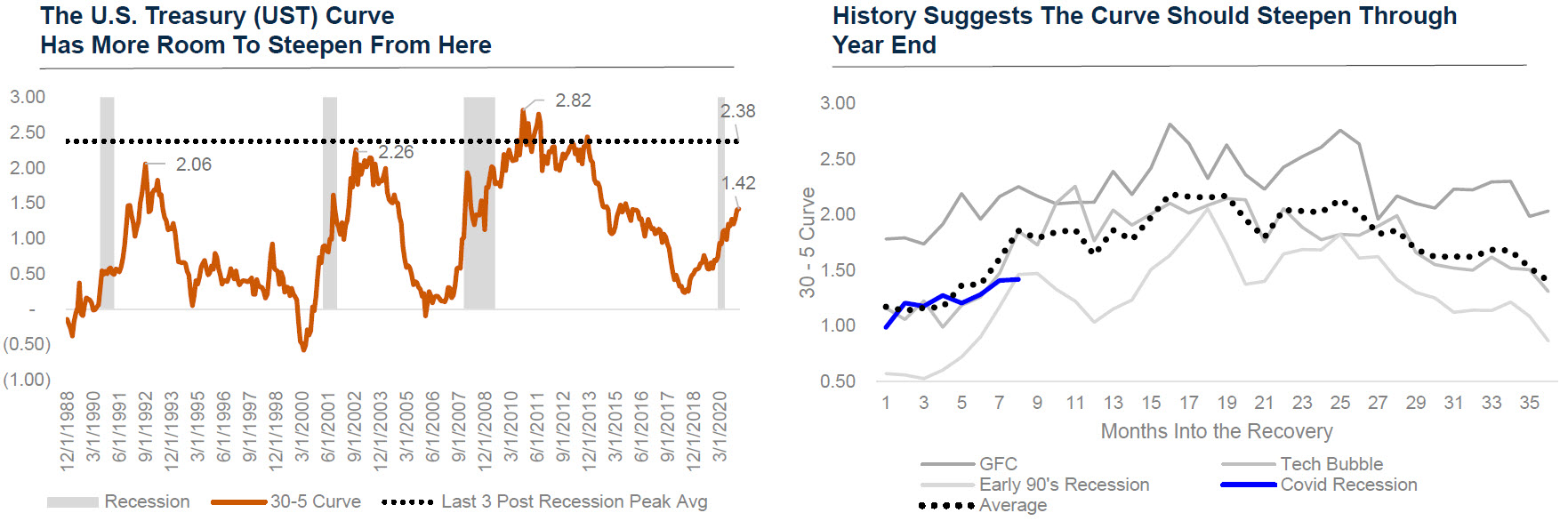

- We believe interest rates will rise further over 2021 driven by inflation expectations and real rates as the market prices a tapering of quantitative easing (QE). Monetary and fiscal authorities are now moving together to drive growth above trend and employment to equilibrium; we are confident that this partnership will push inflation higher in the years ahead.

- We are monitoring the following downside scenarios closely: 1) Interest rates may rise too far too fast; 2) Future COVID-19 variants may reduce vaccine efficacy; 3) Rising corporate tax rates and regulation; 4) Vaccine adoption; 5) The Fed may tighten too quickly; 6) Regulatory risk with Big Tech.

Tactical Asset Allocation & Market Themes

| Equity Markets

Fixed Income

Credit Markets

|

Asset Allocation Views, In Summary…

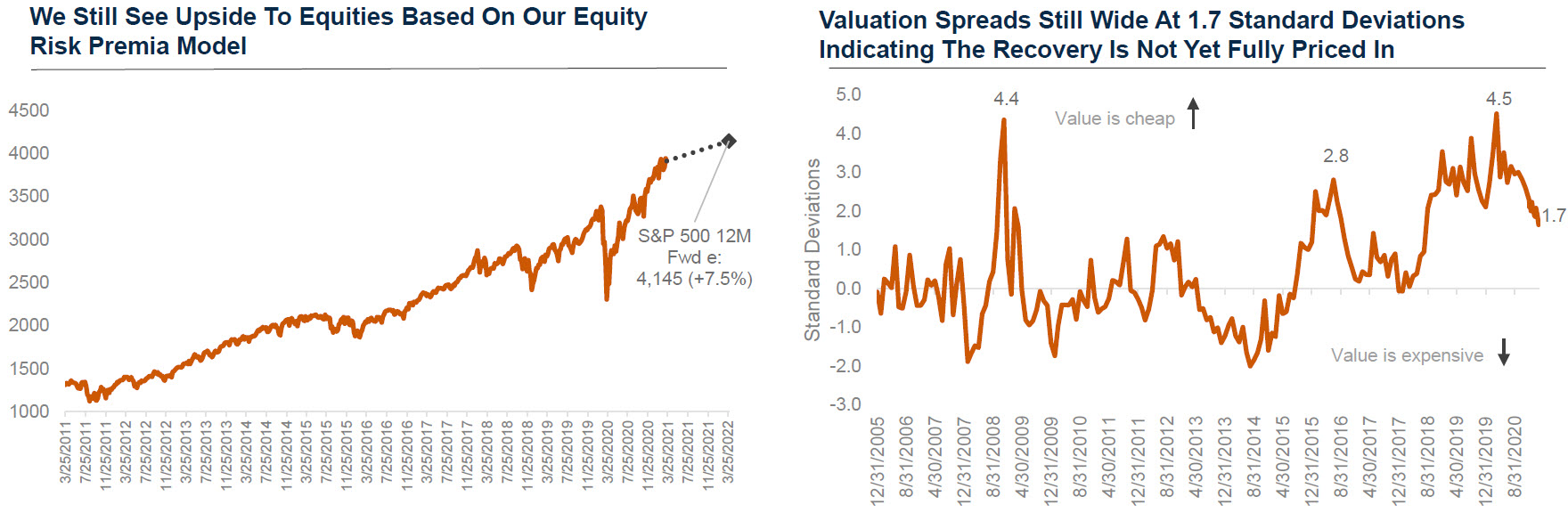

Sources: Harbor MAST U.S. and China BCIs (Top Left), Harbor MAST U.S. Fundamental Real GDP Forecast; Bloomberg; Federal Reserve; Association of American Railroads (Top Right), Harbor MAST BCI Index; Harbor MAST Real GDP Growth Forecast (Bottom Left), UBS Biopharma Analysis (Bottom Right), as of March 2021. See Legal Notices & Disclosures.

Sources: Harbor MAST BCI and Real YOY GDP Forecast as of September 2020 (Top Left), Harbor MAST; Federal Reserve; Bureau of Economic Analysis; Bureau of Labor Statistics; Congressional Budget Office; Bloomberg (Top Right), Harbor MAST; Bureau of Economic Analysis (Bottom Left), Harbor MAST; Bloomberg (Bottom Right), as of March 2021. See Legal Notices & Disclosures.

Sources: Harbor MAST, Bloomberg (Top Left), Harbor MAST; Barra; FactSet (Top Right), Harbor MAST; Barra, FactSet (Bottom Left), Harbor MAST, Bloomberg (Bottom Right) as of December 2020. See Legal Notices & Disclosures.

What Keeps Us Up at Night…

- Rising Corporate Taxes and Regulation

Democrat leadership has signaled a desire to raise corporate, personal and dividend/capital gains tax rates; there has even been discussion of implementing a new wealth tax. These actions would be fiscally restrictive all else equal, and a higher corporate tax rate would affect the value ascribed to U.S. equities. - COVID-19 Variants

As different COVID-19 mutations evolve and form into variant strains of the virus, there is a risk that mortality rises, vaccines become less efficacious, and societies shut down again as new booster shots are formulated to address the new variants. - Vaccine Adoption and Success

We expect the majority of adults in the U.S. to be vaccinated by the summer and in Europe by summer’s end. There is a risk, however, that a sufficiently large part of the population chooses to avoid vaccinations and therefore prevent societies from fully reopening. - Inflation and Rising Rates

With strong above trend growth already in the works for 2021 along with massive fiscal stimulus, it is possible that inflation rises faster than the market currently expects and brings with it nominal rates to much higher levels. This could cause the Fed to act sooner rather than later, both in terms of pulling back on QE but also in terms of signaling a higher Fed Funds rate through the dot plot trajectory. - Fed Mistake

If the Fed chooses to pull back on stimulus too quickly - or send a signal that it’s stimulus and inflationary posture may last shorter than the market expects - it could lead to volatility in rates markets that may then spill over into other asset classes. - Regulatory Risk with Big Tech

The Justice Department has ramped up its Google probe; given the size of Big Tech and their concentration in passive indices, this could have a significant impact on markets.

Legal Notices & Disclosures

The views expressed herein are those of the Harbor Multi Asset Solutions Team at the time the comments were made. They may not be reflective of their current opinions, are subject to change without prior notice, and should not be considered investment advice. These views are not necessarily those of the Harbor Investment Team and should not be construed as such. The information provided is for informational purposes only.

Past performance is no guarantee of future results.

The information shown relates to the past. Past performance is not a guide to the future. The value of an investment can go down as well as up. Investing involves risks including loss of principal.

All investments are subject to market risk, including the possible loss of principal. Stock prices can fall because of weakness in the broad market, a particular industry, or specific holdings. Bonds may decline in response to rising interest rates, a credit rating downgrade or failure of the issue to make timely payments of interest or principal. International investments can be riskier than U.S. investments due to the adverse affects of currency exchange rates, differences in market structure and liquidity, as well as specific country, regional, and economic developments. These risks are generally greater for investments in emerging markets.

Fixed income securities fluctuate in price in response to various factors, including changes in interest rates, changes in market conditions and issuer-specific events, and the value of an investment may go down. This means potential to lose money.

As interest rates rise, the values of fixed income securities are likely to decrease and reduce the value of a portfolio. Securities with longer durations tend to be more sensitive to changes in interest rates and are usually more volatile than securities with shorter durations. Interest rates in the U.S. are near historic lows, which may increase exposure to risks associated with rising rates. Additionally, rising interest rates may lead to increased redemptions, increased volatility and decreased liquidity in the fixed income markets.

Harbor MAST BCI Index Sources: Harbor MAST, Bloomberg, Institute of Supply Management, Federal Reserve, Bureau of Labor Statistics, Commodity Research Bureau, National Federation of Independent Business (NFIB), Caixin, European Commission, Japan Machine Tool Builder’s Association, Association of American Railroads, American Iron and Steel Institute, Department of Labor, Conference Board, University of Michigan, Redbook Research, National Association of Homebuilders, Mortgage Bankers Association

Harbor MAST BCI and Rate of Change Index Sources: Harbor MAST, Bloomberg, Institute of Supply Management, Federal Reserve, Bureau of Labor Statistics, Commodity Research Bureau, National Federation of Independent Business (NFIB), Caixin, European Commission, Japan Machine Tool Builder’s Association, Association of American Railroads, American Iron and Steel Institute, Department of Labor, Conference Board, University of Michigan, Redbook Research, National Association of Homebuilders, Mortgage Bankers Association

2706783

Locate Your Harbor Consultant

INSTITUTIONAL INVESTORS ONLY: Please enter your zip code to locate an Investment Consultant.